by

by By now you’ve heard the news. President Biden dropped out of the 2024 presidential race and paved the way for current VP Kamala Harris to run in his place.

That was big news that shook up the election overnight, and now there is a renewed focus on Harris, including her financial disclosures.

The WSJ ran a story today about how she manages her money, pointing out her penchant for index funds and her ultra-low rate 2.625% mortgage.

I dug a little deeper to see what kind of mortgage she had, along with when and where she got it.

And it turns out it’s an adjustable-rate mortgage, which we all know aren’t for the faint of heart.

Kamala Seems to Really Love the 7-Year ARM

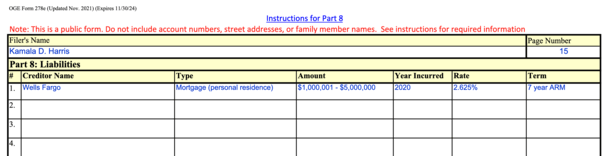

With regard to that 2.625% mortgage Kamala Harris holds, it turns out it’s a 7-year adjustable-rate mortgage (ARM).

This is a popular type of ARM these days because it provides 84 months of interest rate stability before the first adjustment.

In that respect, homeowners can take one out and not worry about their rate increasing for many years.

And in the meantime, either sell their property or refinance the mortgage if need be.

Harris obtained her latest mortgage in 2020 and was able to get a very low interest rate set at 2.625% until the year 2027.

It’s unclear what the exact loan amount is, but it was revealed to be somewhere between $1,000,000 and $5,000,000.

We also know that the lender in question is Wells Fargo, which has had its share of controversies over the past decade, including improper mortgage lock fees.

What’s even more interesting is this isn’t Harris’ first 7-year ARM. A prior financial disclosure revealed that she took out the same type of loan in 2016 as well.

It featured the same exact mortgage rate, 2.625%. And you guessed it, also came from San Francisco-based bank Wells Fargo.

But wait, there’s more! If we go back to 2012, she took out another 7/1 ARM set at an even lower 2.5%.

In total, that’s three 7-year ARMs in a row dating back about 12 years. Based on that timing, you’d expect a fourth around now, but mortgage rates are no longer cheap.

Unfortunately, a typical 7-year ARM might now go for closer to 5% or higher, making it a pretty terrible deal. So until rates improve, she’ll likely be holding onto the 2020 loan.

She’s Got Another Three Years to Figure Out Her Next Move

It’s not uncommon for homeowners to take out ARMs and refinance them over and over into new ARMs.

The logic is that an ARM is typically cheaper than a fixed-rate mortgage, and if you refinance it before it becomes adjustable, you get the upside (lower rate) without any of the downside (higher rate adjustment).

The one caveat is the closing costs each time you refinance, though a no cost refinance can work if rates remain cheap.

There’s also the time aspect, as it can take about a month to get a mortgage, and it can be a pain to go through the process.

But if you don’t mind all that, you can get a cheaper mortgage and allocate the savings elsewhere, such as an index fund.

You also get a smaller payment over time if you refinance into a new 30-year loan term since the loan amount will be smaller thanks to several years of paying it down.

Anyway, it seems Harris employed this strategy for the past decade while mortgage rates hit record lows and it worked out favorably.

However, it appears her next move won’t be as easy now that mortgage rates have more than doubled in the past few years.

Her Mortgage Rate Could Jump to 4.625% in 2027

Come 2027, her 7-year ARM will see its first adjustment, and that means it’ll likely rise from 2.625% to 4.625%.

There are typically caps in place that limit initial movement by 2%, and subsequent adjustments by 2%, with a lifetime cap that can’t be exceeded.

So beyond that first adjustment, it could go even higher than 4.625%, perhaps to 6.625% if the associated mortgage index is still inflated at that time.

Assuming that happens, she’d want out of the loan and into something cheaper.

But if mortgage rates are still high then, it might remain her best option, despite being more expensive than her original loan.

This is the big risk of taking out an ARM vs. a fixed-rate loan. With the latter, you never have to worry about a rate adjustment, though you do pay a premium for that assurance.

If all else fails, there’s always the option to sell the property, which solves the adjustable-rate problem.

And if she’s living in the White House, that might work out just fine.

Read on: Are adjustable-rate mortgages finally a good deal again?

(photo: Gage Skidmore)

Before creating this site, I worked as an account executive for a wholesale mortgage lender in Los Angeles. My hands-on experience in the early 2000s inspired me to begin writing about mortgages 18 years ago to help prospective (and existing) home buyers better navigate the home loan process.

Source link

#Presidential #Candidate #Kamala #Harris #7Year #AdjustableRate #Mortgage