by

by There are many different people involved in the home loan process.

I wrote about this in detail already, but probably didn’t even include everyone.

Because getting a mortgage is a pretty big deal, a lot of hands are needed to ensure it goes according to plan.

There are also several ways to obtain a home loan, which require different participants.

For example, if you choose to use a mortgage broker to get your loan, an “account executive” will be in the mix.

The Role of a Mortgage Account Executive

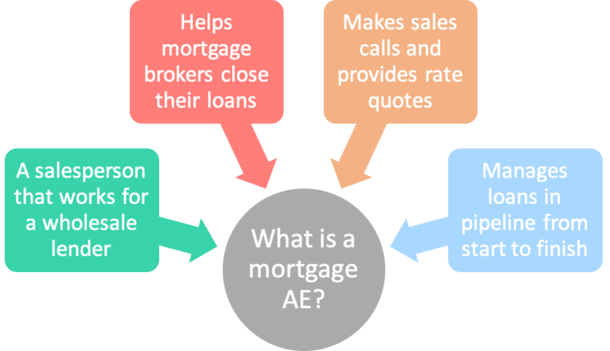

A mortgage account executive, or AE for short, works as a liaison between a mortgage broker and the wholesale lender they represent.

With regard to mortgage lending, wholesale simply means business-to-business (B2B) instead of retail, which is direct-to-consumer (B2C).

Simply put, AEs are NOT consumer-facing and have no interaction with borrowers whatsoever.

Instead, they communicate with the mortgage broker, who in turn corresponds with the borrower.

Typically, AEs hold an internal role at the wholesale lender they represent, meaning they don’t leave the office unless they’re doing a sales pitch.

They simply field phone calls from third-party mortgage brokers and work with their staff internally to originate and close loans.

Mortgage brokers rely on AEs to get loan pricing, submit loans to underwriting, clear conditions once approved, provide status updates, and eventually fund their loans.

In a way, they act similarly to a retail loan officer, but deal with another mortgage professional as opposed to a consumer.

What a Typical Day Looks Like for a Mortgage AE

I worked as an Account Executive in the early 2000s, so I can provide some personal insight here.

Generally, mortgage AEs work regular banking hours, such as 8am to 5pm daily. Perhaps staying late on days that are super busy.

On a typical day, an AE will look over loan files that are already submitted to underwriting and approved.

They will determine what conditions are outstanding to get them to the next step, whether it’s drawing loan documents to be signed or funding the loan.

At the same time, AEs are salespeople. This means they need to make a lot of outgoing phone calls to mortgage brokers to drum up new business.

On these phone calls, they will ask brokers if they have any loan scenarios that need to be priced out.

And if so, will provide mortgage rate pricing in the hopes the broker will like what they hear and send the loan to them.

Assuming that happens, the AE will need to organize the file by collecting necessary paperwork, order a credit report, upload a loan application, and get the whole package over to the loan underwriter.

Once the underwriter decisions the file, they will get in touch with the broker, and if approved, send them a list of prior-to-doc (PTD) conditions.

Again, they’ll need to facilitate this paperwork collection process, ensure that a home appraisal is ordered, and provide status updates along the way.

What they communicate to the broker will be shared with the borrower and everyone will work together to close the loan in a timely fashion.

The Job Is Sales and Operations Rolled into One

As you can see, a mortgage AE needs to be both a salesperson and a member of the operations staff.

They need to bring in new business and oversee their loan pipeline to ensure the mortgages in process make it to the finish line.

This means being a good communicator, staying organized, having good time management skills, and the ability to put out fires when they inevitably surface.

Mortgages rarely go completely according to plan, so AEs will need to step in to offer solutions, save files, make hard phone calls, and more.

If an appraisal comes in low, they’ll need to call the broker and work on a new plan to make the loan work.

Similarly, if something turns up during the underwriting process, they may need to get creative to keep the file in good standing and push forward.

And remember, while all of this is happening, they still need to generate new business. It’s a bit of a juggling act and it can be very stressful.

To make matters worse, there are often quotas to meet each month to ensure they make top dollar for the work that they do.

How Do Mortgage AEs Get Paid?

The company I worked for paid both a base salary and commission on loans closed during the month.

The base salary was very low, but still provided assurances that you wouldn’t walk away with nothing.

However, it was ultimately the commission where you could make the most money. And it was all dependent on how many loans you closed each month.

Those who were able to close above a certain dollar amount each month were entitled to a bigger cut.

So you were incentivized to fund more loans. This was also very stressful, as closing an amount below a certain threshold could reduce your take home salary substantially.

For example, if you funded below X dollars, you may have only been paid a flat fee per loan. But if you funded above X dollars, you’d get a percentage that amounted to a lot more money.

Nowadays, mortgage companies may pay AEs a higher per-loan commission but not provide a base salary. This can be a great tradeoff if you close a lot of loans.

Conversely, those who accept a base salary may not make as much per loan, despite the guaranteed salary.

At the end of the day, being an AE isn’t much different than being a retail loan officer.

The main difference is you work for a wholesale lender and interact with mortgage brokers instead of homeowners and/or home buyers.

There are pros and cons depending on who you ask. Sometimes it can be easier to deal with another mortgage professional as opposed to say a first-time home buyer, for obvious reasons.

Source link

#Mortgage #Account #Executive